Dear Readers:

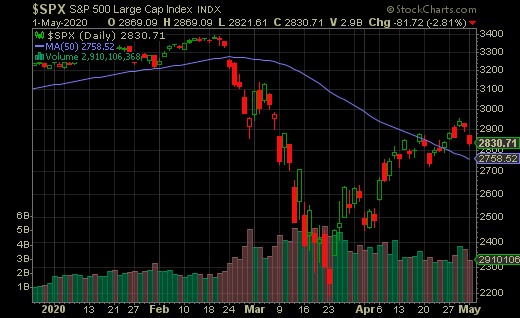

Friday we kicked off May trading with a broad sell-off on the major indexes, erasing gains made earlier in the week. Lack of volume shows less fervor for the Bears.

The month of April proved to be the best for the S&P 500 since 1987 as it rocketed up 12.7%, cutting its loss for the year to 10%.

The Coronavirus appears to be slowing. States are either re-opening or making plans to do so. All great news minus the fear of infections with a second wave which will persist until a vaccine is available.

Heavy-handed short covering has fueled upward momentum. This rally off the March low doesn’t look any different than a bear market rallies following similar steep sell-offs.

Buyers are more concerned with going against the government’s massive stimulus than focussing on the usual fundamentals.

Unfortunately, economic carnage from stay-at-home orders is feared to be among the worst the United States has seen, though only time will tell. First quarter GDP fell 4.8%, but the second quarter is estimated to have a 30% to 40% drop, with full year GDP expected to contract 4% to 5%.

Widespread struggling among companies will continue. Earnings are expected to fall more than 15% for the first quarter. More than 30 million people have lost their jobs in the last six weeks.

Quarterly reports from the digital heavyweights showed some resilience with sales and are poised to do well with their work-from-home products. Thought future guidance was lacking.

Apple (AAPL), +2.16%, showed resilience with iPhone sales, though declined to give guidance. Google (GOOG), +3.23%, had better than expected revenue, search biz stable, cloud biz more appealing to CEO’s, work at home. Microsoft (MSFT), +0.01%,reported it was alive and well, a boost from its XBox home video game a highlight.

Pandemic success Amazon (AMZN), -5.15%, said it would spend its $4B profit to help protect its workforce from Covid-19, including $1B for in-house testing. While its cloud business slowed, its video conference, gaming and entertainment picked up. Amazon’s stock is up more than 50% since its March low.

Technically Speaking

- The S&P 500 holds above its 50-day simple moving average.

- Volume patterns continue to favor the bulls, though it may be short covering and stimulus related rather than truly committed buyers. Six clear Accumulation Days have been notched in since the March low, where the Bears have failed to notch in a single Distribution Day

Small caps are showing relative strength with the S&P Smallcap 600 up 3.48% for the week. Materials and Energy were big gainers here, a sign of optimism as the larger companies have been seen as safer for investors compared to the riskier, more leveraged small companies.

The market will become more selective over stocks with a flight to quality. Growth stocks prefer bull markets to move them higher. Few from this group tend to do well when the trend is down.

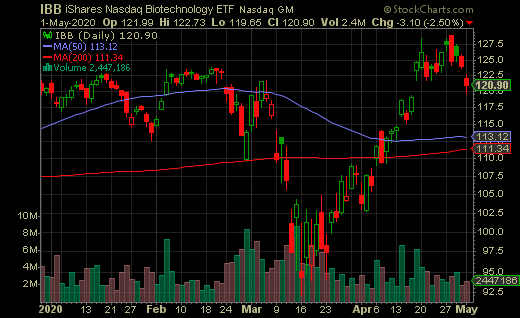

The Nasdaq Biotechnology Index (IBB) fell 4% and back below its breakout base line as it put the breaks on a strong rally that began mid-March. The sector remains in the spotlight with hopes of a remedy and cure for the virus.

Gilead Science’s (GILD), +0.39%, Remdesivir showed positive testing results with about a thousand Covid patients, reducing their hospital stays by about four days on average to 11. Any hint that they’re on the right track with this could serve as a base for other drugs.

Intact breakouts in biotech include Cel-Sci Corp. (CVM), United Therapeutics Corp. (UTHR), Repligen Corp. (RGEN), Bio-Techno Corp (TECH) and Vertex Pharmaceuticals (VRTX.)

Heavyweight Amgen (AMGN) looks to be tested with its breakout, failing is BioMarin (BMRN.)

The economy is changing. It may be rough sledding at the moment, though we will come out of it stronger and better. This report will have much to say on trends shaping our lives and investments. There’s loads of opportunity.

And, there’s plenty of chicken to make up for a decline in red meat.

Good luck out there,

Dan